The TSP Roth In-Plan Conversion: A Game-Changer for Federal Employees

Starting January 28, 2026, federal employees with a Traditional TSP balance gained a powerful new tool: the ability to convert pre-tax savings directly to Roth — inside the plan itself, with no outside rollover required. Here is everything you need to know.

What Is a Roth In-Plan Conversion?

A Roth in-plan conversion moves money from your Traditional (pre-tax) TSP balance into your Roth (after-tax) TSP balance. The converted amount is taxed as ordinary income in the year the conversion takes place. In exchange, that money — and all its future growth — can be withdrawn tax-free in retirement, provided you meet IRS rules.

Before this option existed, federal employees who wanted to shift Traditional TSP funds into a Roth account had to roll over to a Traditional IRA first, then convert to a Roth IRA — a cumbersome two-step process available only to separated employees or those who had reached age 59½. The new in-plan conversion eliminates those obstacles. Active employees at any age can now convert.

How It Works: The Key Details

The Federal Retirement Thrift Investment Board published the final rule on January 15, 2026. Here are the mechanics:

- Who is eligible: Active employees, separated participants, and spousal beneficiaries who have a vested Traditional TSP balance may request a conversion.

- Minimum conversion amount: $500 per transaction.

- Frequency: Up to 26 conversions per calendar year — one for each biweekly pay period if desired.

- How to request: Through the "My Account" section at tsp.gov, either as a specific dollar amount or a percentage of your eligible balance.

- Balance retention: You must generally retain at least $500 in each applicable tax-deferred contribution source after converting.

- Mutual fund window: Funds invested through the TSP mutual fund window must first be moved back into the core TSP funds before conversion.

The Tax Consequences You Need to Understand

The trade-off is straightforward: you pay taxes now in exchange for tax-free income later. When you convert Traditional TSP funds, the converted amount is added to your gross income for that tax year. A $30,000 conversion, for example, is taxed at your ordinary income rate — and could push you into a higher bracket if not managed carefully.

⚠ Important Tax Detail

There is no automatic tax withholding on TSP in-plan conversions. You will likely need to make estimated quarterly tax payments to avoid underpayment penalties. If your conversion falls in the first quarter (January 1–March 31), the federal estimated payment is due April 15. The taxes must be paid from personal funds outside your TSP account — you cannot use your TSP balance to cover the bill.

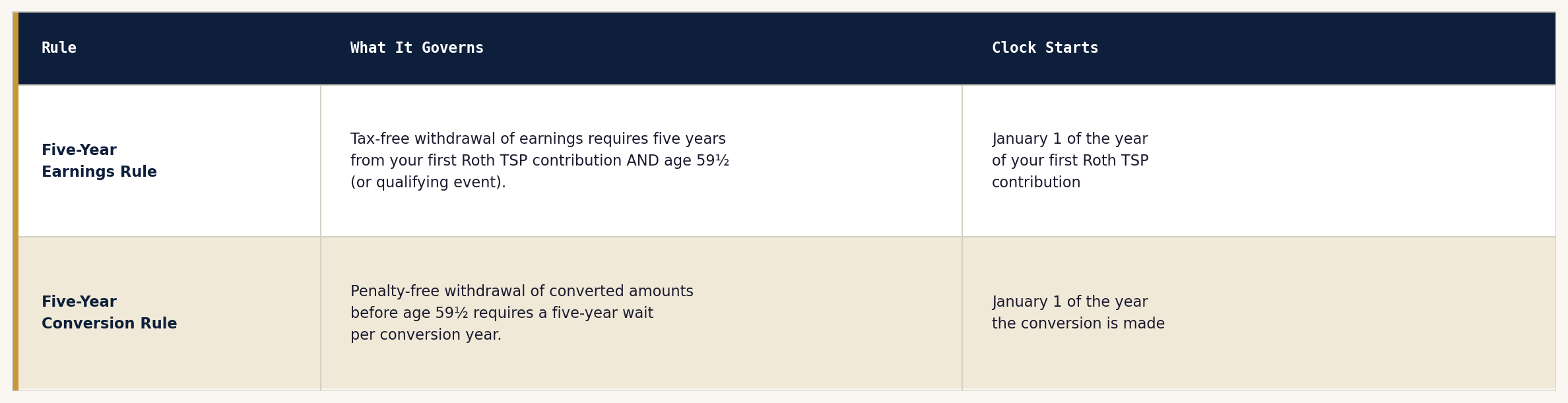

The Five-Year Rules: Pay Close Attention

Roth TSP accounts are subject to two distinct five-year rules. In-plan conversions add a layer of complexity worth understanding clearly before acting.

Practically speaking: if you convert in 2026 and are under age 59½, you generally cannot withdraw that converted amount penalty-free until January 1, 2031. For most federal employees at or near retirement age who are already 59½ or older — and have held a Roth TSP for at least five years — this restriction will not apply.

A well-timed series of smaller conversions over several years almost always outperforms a single large conversion — both for your tax bracket and for managing Medicare premiums.

Who Should Consider a Roth In-Plan Conversion?

This strategy is not right for everyone, but it can be especially powerful in several situations common to federal employees:

- You expect higher taxes in retirement: Federal employees with FERS pensions, Social Security, and large TSP balances often land in surprisingly high brackets in retirement. Converting now at a lower rate locks in real savings.

- You want to reduce Required Minimum Distributions: Traditional TSP balances trigger RMDs beginning at age 73. Reducing that balance through Roth conversions directly lowers your future RMD obligations. And since 2024, Roth TSP balances are no longer subject to RMDs during your lifetime; converted funds stay in the Roth TSP free of mandatory distributions.

- You are in a temporarily low-income year: The year you retire, transition, or experience an income gap can be an ideal window to convert at a lower marginal rate.

- You want to manage IRMAA exposure: Roth TSP withdrawals do not count as taxable income, which can help reduce your Modified Adjusted Gross Income (MAGI) and potentially lower Medicare Part B and Part D premium surcharges.

A Related Change: Roth-Only Catch-Up Contributions for High Earners

Alongside in-plan conversions, a second major Roth change took effect January 1, 2026 under the SECURE 2.0 Act of 2022. Federal employees age 50 or older whose 2025 Medicare wages (Box 5 of their W-2) exceeded $150,000 are now required to direct all catch-up contributions to the Roth TSP — not the Traditional TSP.

For 2026, the catch-up limit is $8,000 for those aged 50–59 and 64+, and $11,250 for those aged 60–63. This mandatory Roth catch-up applies only to contributions above the standard $24,500 elective deferral limit. Your regular contributions can still be split between Traditional and Roth as you choose — only the catch-up portion is affected for high earners.

Example Impact

A 55-year-old GS-14 earning $165,000 who contributes the full catch-up of $8,000 will now do so with after-tax dollars. At a 24% federal bracket, that's roughly $1,920 more in federal taxes for the year — but those funds will grow and withdraw tax-free in retirement.

Practical Steps Before You Convert

- Review your current and projected tax brackets. A conversion makes the most sense when your current rate is lower than what you expect to face in retirement.

- Confirm you have sufficient liquid funds outside your TSP to pay the resulting tax bill. Do not attempt a large conversion if you cannot comfortably cover the liability from personal savings.

- Consider a laddered approach — spreading smaller conversions across multiple years — rather than one large conversion, to stay within a favorable bracket.

- Be mindful of IRMAA thresholds if you are at or near Medicare age. A large single-year conversion can trigger or increase Medicare premium surcharges two years later.

- Use the TSP's forthcoming conversion estimator once it becomes available to model potential tax impacts before committing.

The Bottom Line

The TSP Roth in-plan conversion is one of the most significant retirement planning enhancements federal employees have seen in years. It gives you greater flexibility to manage your tax burden in retirement, reduce RMD obligations, and potentially lower your Medicare premiums — all without leaving the TSP.

But it is not a one-size-fits-all strategy. The decision to convert, how much to convert, and when to do it should be driven by a careful analysis of your income today, your expected income in retirement, your tax bracket, and the liquid assets you have available to cover the tax bill.

As a financial planner who works exclusively with educators and public service professionals, I am here to help you evaluate whether a Roth in-plan conversion makes sense for your specific situation. If you would like to explore your options, please reach out to schedule a consultation.

Disclaimer: This post is for educational purposes only and does not constitute personalized tax or financial advice. Tax rules are complex and individual situations vary. Please consult a qualified tax advisor or financial planner before making any retirement account decisions. Chris Reddick Financial Planning, LLC is registered with the Texas Securities Board.